Liquid Funds

Apart from bank deposits, there is an even more lucrative option to meet your short-term investment needs -- liquid mutual funds. Let’s explore what liquid funds are, how they work and if you should invest in them.

What is Liquid Fund?

Liquid fund is a debt mutual fund that invests in high-quality debt securities, with a short maturity period of up to 91 days. These funds invest in money-market securities like treasury bills, commercial papers, and certificates of deposit of very short durations.

These mutual funds are a great avenue to park any surplus cash as they focus on two things – providing easy access to your money (liquidity) and preserving capital – making them a low-risk investment option. They are ideal for short-term investors who want to park their funds for a few days to a month.

Liquid funds’ returns depend on the market prices of the money-market instruments they have invested in. Since short-term securities are less volatile than long-term securities, liquid funds carry the lowest interest rate risk in the debt mutual fund category.

You can redeem units of a liquid fund in T+1 day. Apart from safety and liquidity, these funds can offer a higher post-tax return than savings bank accounts, making them an attractive alternative.

A good liquid fund has characteristics like a low expense ratio, high credit quality of the portfolio, and a disciplined investment approach.

Sort by

AUM ₹1366 Cr •

Expense 0.16%

AUM ₹47855 Cr •

Expense 0.21%

AUM ₹4473 Cr •

Expense 0.07%

AUM ₹1657 Cr •

Expense 0.1%

AUM ₹475 Cr •

Expense 0.12%

AUM ₹34674 Cr •

Expense 0.15%

AUM ₹11193 Cr •

Expense 0.17%

AUM ₹6246 Cr •

Expense 0.08%

AUM ₹7187 Cr •

Expense 0.13%

AUM ₹18782 Cr •

Expense 0.12%

AUM ₹15673 Cr •

Expense 0.09%

AUM ₹25219 Cr •

Expense 0.16%

AUM ₹32108 Cr •

Expense 0.2%

AUM ₹22304 Cr •

Expense 0.1%

AUM ₹3774 Cr •

Expense 0.12%

AUM ₹13774 Cr •

Expense 0.12%

AUM ₹2249 Cr •

Expense 0.13%

AUM ₹23123 Cr •

Expense 0.2%

AUM ₹10694 Cr •

Expense 0.16%

AUM ₹13223 Cr •

Expense 0.15%

Apart from bank deposits, there is an even more lucrative option to meet your short-term investment needs -- liquid mutual funds. Let’s explore what liquid funds are, how they work and if you should invest in them.

What is Liquid Fund?

Liquid fund is a debt mutual fund that invests in high-quality debt securities, with a short maturity period of up to 91 days. These funds invest in money-market securities like treasury bills, commercial papers, and certificates of deposit of very short durations.

These mutual funds are a great avenue to park any surplus cash as they focus on two things – providing easy access to your money (liquidity) and preserving capital – making them a low-risk investment option. They are ideal for short-term investors who want to park their funds for a few days to a month.

Liquid funds’ returns depend on the market prices of the money-market instruments they have invested in. Since short-term securities are less volatile than long-term securities, liquid funds carry the lowest interest rate risk in the debt mutual fund category.

You can redeem units of a liquid fund in T+1 day. Apart from safety and liquidity, these funds can offer a higher post-tax return than savings bank accounts, making them an attractive alternative.

A good liquid fund has characteristics like a low expense ratio, high credit quality of the portfolio, and a disciplined investment approach.

Features of Liquid Funds

Here are the main characteristics of liquid funds:

High Liquidity: Liquid funds, as their name suggests, offer high liquidity, allowing investors to withdraw their money at short notice, generally in 24 hours.

Low Risk: Liquid mutual funds are safer than other debt funds as they have a lower interest rate risk due to the shorter maturity of underlying securities.

No Exit and Entry Load: Typically, a liquid mutual fund does not carry an entry or exit load as it is designed to be highly liquid and provide quick access to funds. Only redemption within seven days attracts a small exit load.

Alternate to savings bank account: Historically, liquid funds have provided returns in the range of 7-9%, which are significantly better than interest rates offered by savings accounts, making them a good alternate investment option.

How Do Liquid Funds Work?

To understand liquid funds better, it's important to know where they invest and how they generate returns.

Where do liquid funds invest?

Liquid funds invest in high-quality, short-term, and highly-liquid debt instruments. As per the recent guidelines by the market regulator Securities and Exchange Board of India (SEBI), liquid funds must primarily invest in listed commercial papers, while limiting exposure to a single sector to 20%. They cannot invest in high-risk assets as per SEBI rules to keep credit risk in check.

Furthermore, liquid funds must hold at least 20% of their assets in cash and cash equivalents to ensure they can fulfil redemption requests quickly.

How do liquid funds make money?

A liquid fund typically earns money through interest on debt investments with only a small portion of earnings coming from capital gains.

In the debt market, when interest rates fall, bond prices rise and when rates go up, bond prices fall. This inverse relation is more pronounced in long-term bonds. Since liquid funds invest in short-term securities, their market value doesn’t fluctuate much with interest rate changes as compared to long-term debt funds.

In times of rising interest rates, liquid funds often perform better than other debt funds. This is because their interest income increases and their value doesn’t drop much. Therefore, liquid funds face lower risk from changes in interest rates.

Advantages of Liquid Funds

Here are the advantages of investing in liquid funds:

Low Risk: The fund managers of liquid funds are focused on the preservation of capital and generating stable returns. These funds invest in high-quality securities with short-term maturity of up to 91 days, making them less exposed to volatility.

Low Cost: Liquid funds are not as actively managed and generally have an expense ratio of less than 1%. This low-cost structure offers investors a promising investment return.

Flexibility: Liquid funds have a flexible holding period, meaning you can enter and exit your investments without any hassle. However, an exit load is applicable on redemption within seven days of allotment of units.

Easy Redemption: Redemption requests for liquid funds are usually processed within one working day. Additionally, some funds offer the option of instant redemption.

Risks of Investing in a Liquid Fund

While a liquid fund has many advantages, it also carries certain risks like:

Credit Rate Risk: Despite investing in high-quality, short-term securities, there’s always a chance that the issuers of the debt instruments held by the liquid fund might default on their interest payments. This will impact the mutual fund's returns and net asset value (NAV).

Interest Rate Risk: A liquid fund is prone to interest rate fluctuations as it invests in debt instruments. Any significant change in the interest rate can impact the value of the securities held by the fund. However, this risk is lower in liquid funds.

Who Should Invest in Liquid Funds?

Liquid mutual funds offer a mix of stable returns, liquidity and safety. Here are the types of investors who can consider investing in liquid funds:

Short-term investors: Liquid funds are suitable for investors seeking reasonable, low-risk returns, and having a short-term investment horizon of up to 3 months. For an investment horizon of up to 6 months or a year, investors can consider longer duration funds as they can offer higher returns.

Investors looking to park funds temporarily: According to experts, if you have a sudden influx of cash, for example, from a huge bonus or sale of real estate, and you are unsure how to use that money, liquid funds can be a great parking ground. These funds will ensure the safety of your corpus while generating a small return on it.

Investors seeking alternatives to bank deposits: Retail customers who keep their funds in savings accounts can consider liquid funds as they offer higher returns. A fixed deposit has a lock-in period, and a penalty is imposed on withdrawal before maturity. On the other hand, liquid funds give easy exit options and have flexible holding periods.

Investors who want to create a contingency fund: Investors can use liquid funds as a contingency or emergency fund since these funds are less prone to credit risk on the back of investments in short-duration securities. Moreover, you can redeem your units easily.

Investors transitioning to equity funds: Investors seeking opportunities in equity funds often park their money in liquid funds temporarily while they wait for the right investment opportunity. Apart from this, many investors use liquid funds to gradually transfer their investments into equity mutual funds through a Systematic Transfer Plan (STP), as they believe this method could generate higher returns.

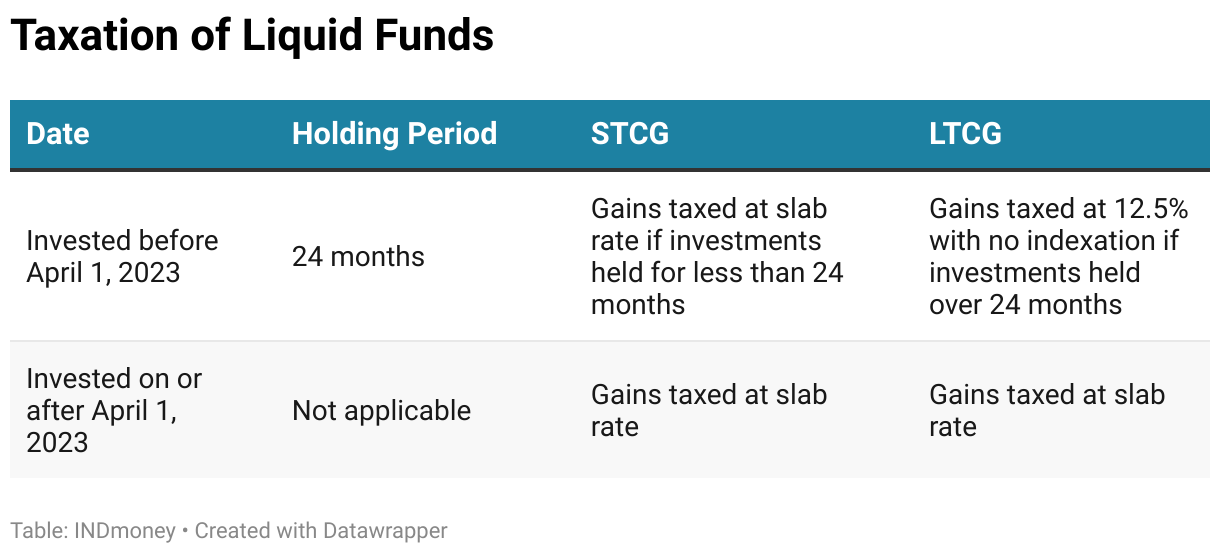

Taxation Rules on Liquid Mutual Funds

Liquid funds can offer good returns to investors. However, it is important to understand how they are taxed. For investments made after April 1, 2023, gains from debt funds are taxed at your income tax slab rate.

Investments made in liquid funds before April 1, 2023, are taxed as per the holding period. Here are the details:

Short-term Capital Gains Tax (STCG)

If you hold your liquid funds for less than 24 months, the gains are categorised as short-term capital gains. They are taxed as per your income tax slab.

Long-term Capital Gains Tax (LTCG)

If you hold your liquid funds for more than 24 months, the gains are categorised as long-term capital gains. They are taxed at 12.5%.

Tax on Dividends

Dividends from liquid funds are taxable in the hands of investors at their applicable slab rate from the financial year 2020-21. A TDS of 10% applies if dividends from a single asset management company exceed ₹5,000 in a financial year.

How to Invest in Liquid Mutual Funds

Investors can invest in the best liquid mutual funds easily through INDmoney’s app in a few easy steps:

- Open the INDmoney app and log in with your credentials.

- Navigate to the "Mutual Funds" section within the app.

- Use the filter options to select "Liquid Funds" to view the available choices.

- Choose between a lump sum investment or a Systematic Investment Plan (SIP) for regular investments.

- Enter the amount you wish to invest and confirm the transaction.

Frequently Asked Questions

Liquid funds are debt funds that invest in high-quality, short-term money market instruments with a maturity of up to 91 days.

While investing in a liquid fund consider factors like assets under management, expense ratio, fund manager’s acumen, historical performance and objective of the fund.

Typically, FDs and liquid funds offer similar returns to investors. However, unlike FDs, you don’t have a lock-in period for liquid funds and can redeem them after seven days without attracting any exit load.

Yes, you can opt for SIP in a liquid mutual fund by selecting the frequency of your investment. Once done, the money will automatically get deducted from your bank account and invested in the fund of your choice.